India's SMB ecosystem is suffocating under a hidden crisis: working capital starvation. Large buyers — retailers, manufacturers, hospital chains, hospitality groups — demand 60-90 day payment terms. But their suppliers (SMBs) must pay workers, buy raw materials, and fulfill orders immediately. This timing mismatch creates a $500 billion gap that no traditional bank has solved.

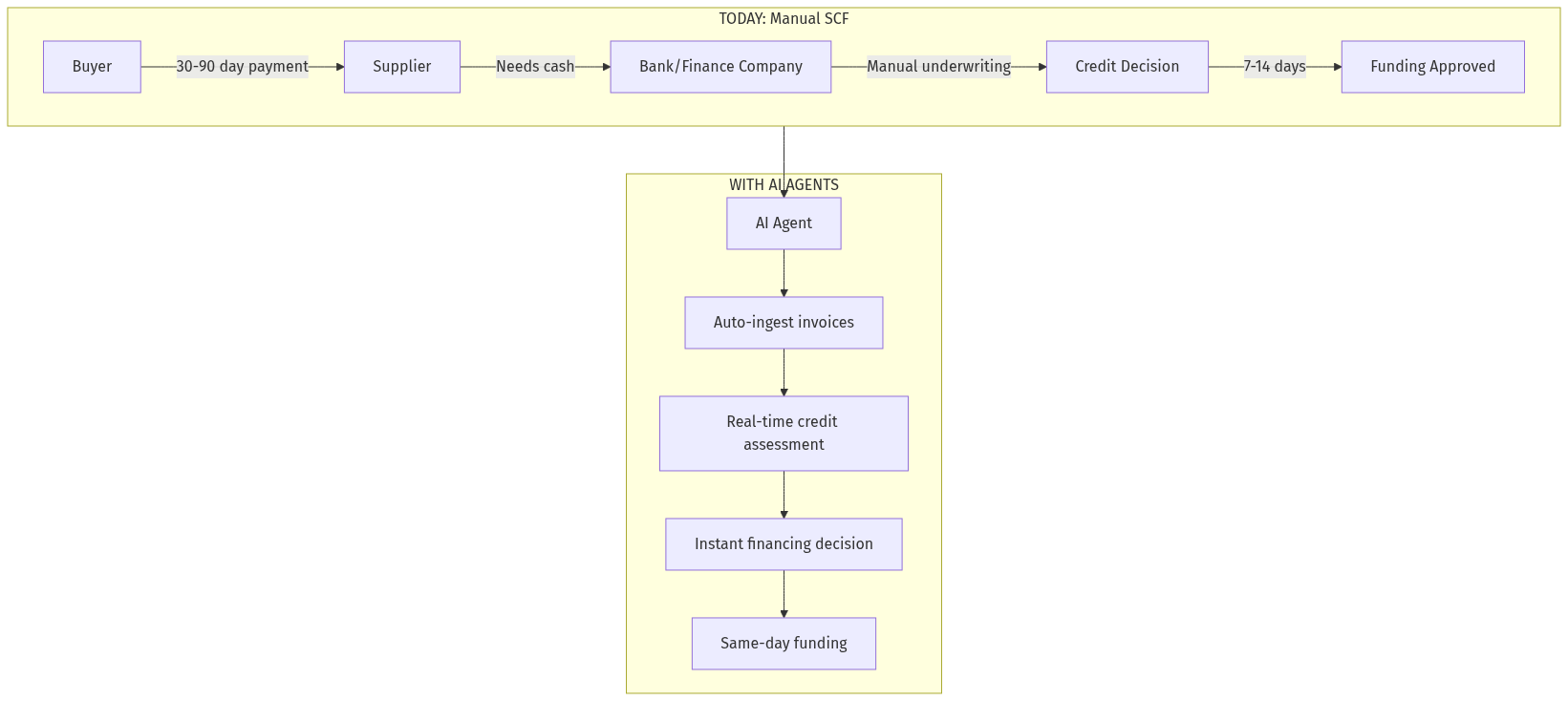

Supply Chain Finance (SCF), also known as reverse factoring, solves this by allowing buyers to validate supplier invoices, enabling financiers to pay suppliers early at rates tied to the buyer's credit rating (not the supplier's). But SCF in India remains limited to large corporations with dedicated treasury teams. SMBs are excluded.

This article presents the opportunity to build an AI-powered SCF platform that:

- Auto-discovers invoice opportunities from e-invoicing data

- Provides instant credit decisions using alternative data

- Enables same-day financing for approved invoices

- Reduces financing costs by 40-60% vs current informal lending