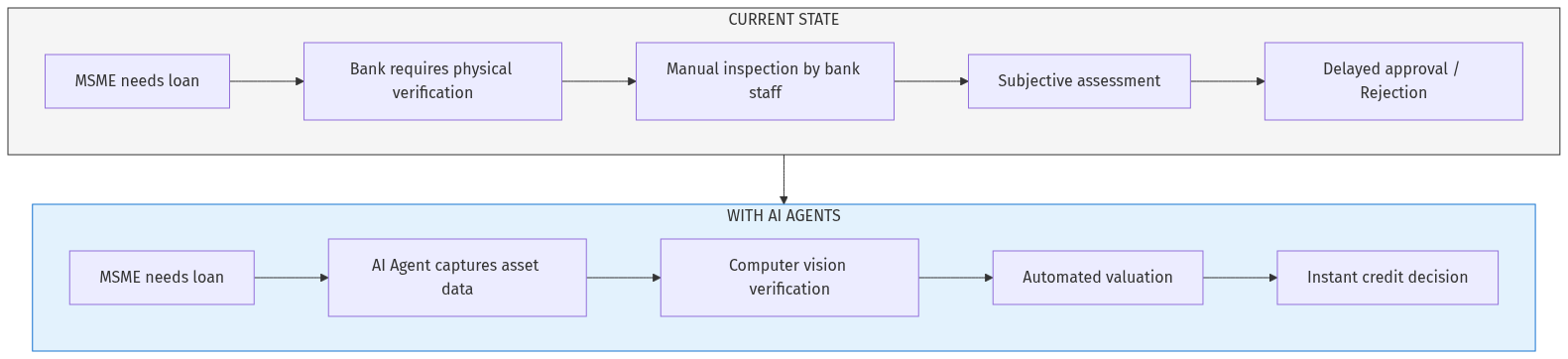

India's MSME sector contributes 30% to GDP and employs 110 million people, yet faces a massive credit gap of $530 billion. The primary bottleneck is collateral verification — a manual, subjective, and time-consuming process that takes 15-45 days and has a 70% rejection rate.

This article explores the opportunity to build AI-powered asset verification platforms that use computer vision, IoT sensors, and automated valuation models to replace physical inspections. The solution can reduce verification time from weeks to hours, increase approval rates by 40%, and create a proprietary data moat around MSME asset inventories.