India's B2B debt recovery market is broken in a way that destroys more businesses than any competitor or market fluctuation. When a large buyer delays payment to a small supplier, the supplier has limited options: negotiate personally (awkward), hire a lawyer (expensive), engage a collections agency (reputation risk), or write it off (business death).

The result? India's MSMEs lose an estimated ₹5-8 lakh crore annually to payment delays and defaults. Meanwhile, banks and NBFCs write off ₹1 lakh crore+ in bad debts each year. The gap between these numbers represents massive inefficiency.

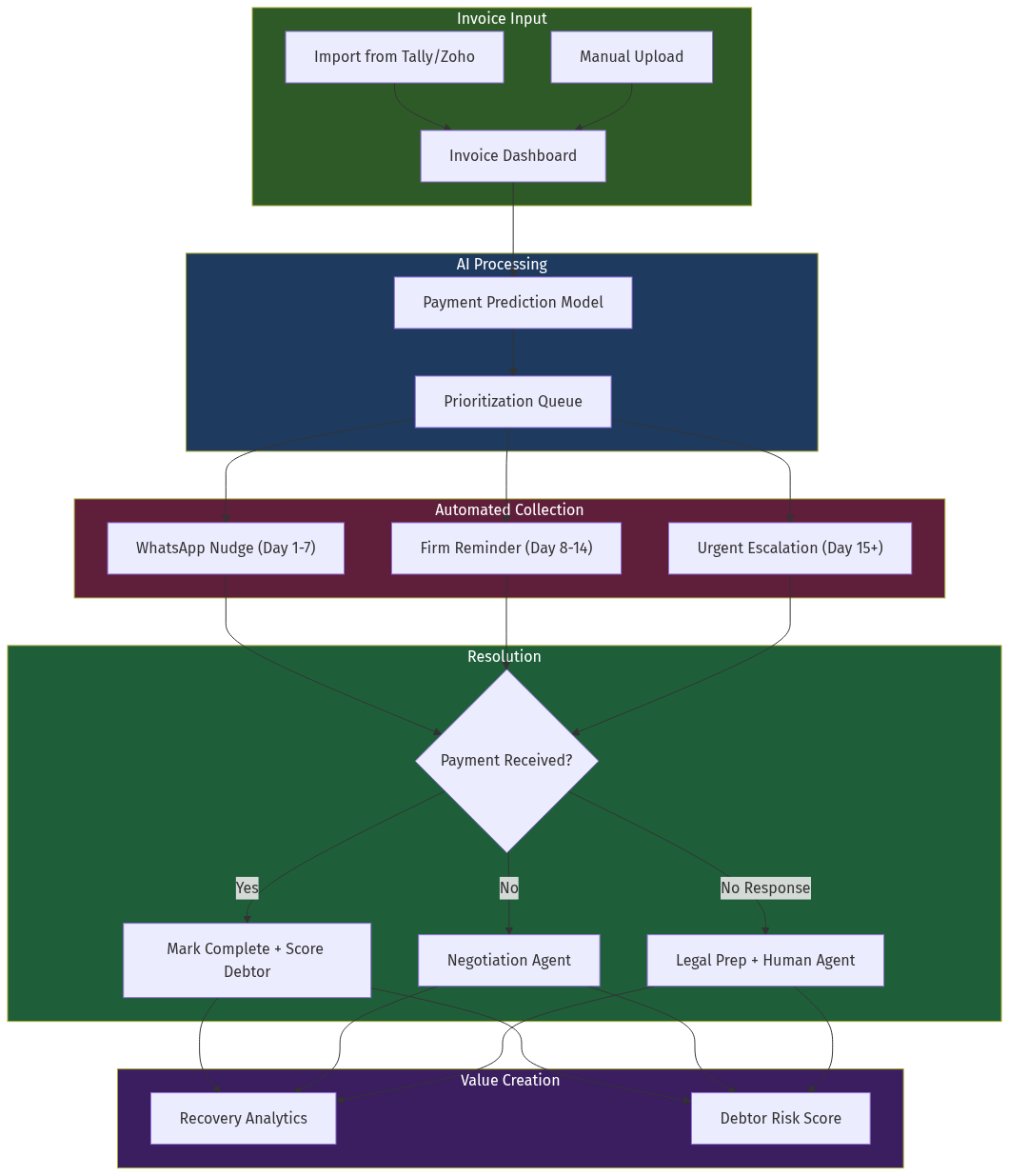

The opportunity: Build an AI-powered B2B collections platform that:The market is ₹10,000+ crore in fees annually, with near-zero digital penetration.