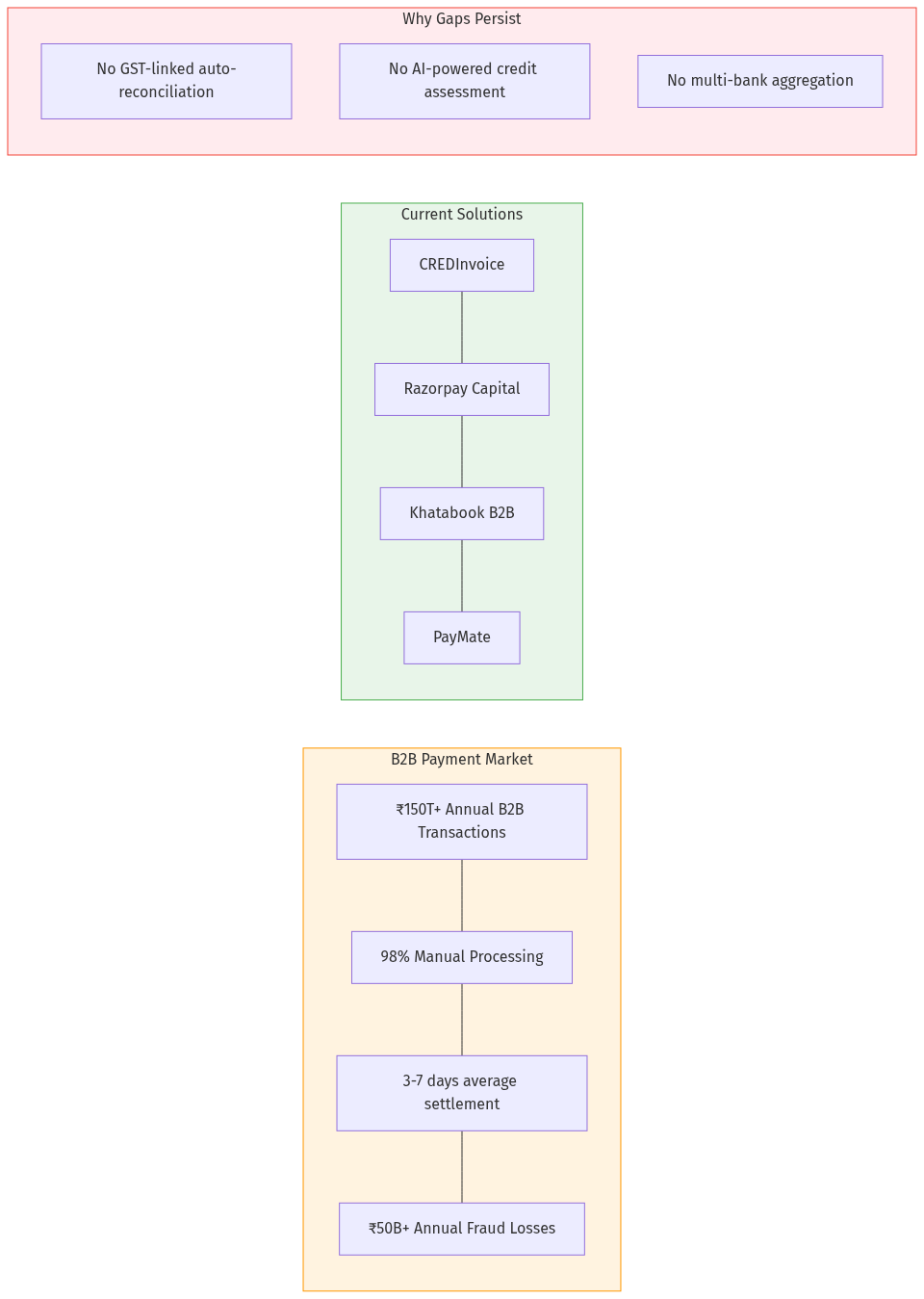

India's B2B payments infrastructure is broken in ways that seem impossible in 2026. While UPI revolutionized consumer payments (2 billion transactions monthly), B2B payments remain stuck in the dark ages — PDF invoices, manual bank transfers, 3-7 day settlement times, and zero automation between payment and accounting.

This is a $150 trillion+ annual opportunity waiting to be restructured. AI agents can now:

- Parse unstructured invoices automatically

- Verify GST compliance in real-time

- Assess credit risk using alternative data

- Trigger payments based on smart contracts

- Reconcile transactions across multiple banks